Introduction to De Minimis

The term ‘de minimis,’ derived from the Latin phrase meaning “about minimal things,” has significant implications within various sectors, particularly in the domains of tax law and financial regulations. In essence, it refers to benefits or amounts that are so trivial that they do not warrant consideration or action. In the context of Philippine employment, de minimis benefits play a crucial role in determining compensations that are exempt from tax liabilities, thereby facilitating a more seamless financial operation for both employers and employees.

In the Philippines, the concept of de minimis was formally recognized in revenue regulations, serving as a guideline for what constitutes minimal benefits within an employment context. For businesses operating in the Philippine market, understanding these de minimis benefits is vital. According to the Bureau of Internal Revenue (BIR), specific allowances that fall under this category are considered non-taxable, allowing both the organization and its employees to engage in enhanced productivity without the burden of additional taxes. Examples may include transportation fare subsidies or meal allowances provided to employees, which are typically essential but may not constitute a significant portion of overall compensation.

The application of de minimis benefits significantly influences employer-employee relationships and impacts overall employee benefits structures. By delineating which allowances can be categorized as de minimis, businesses can offer financial incentives that not only comply with local taxation policies but also foster a positive work environment. As such, de minimis regulations are not merely legal stipulations; they reflect a broader commitment to fair and equitable labor practices within the Philippine employment landscape, ultimately affecting overall workplace satisfaction and productivity.

Overview of Revenue Regulations No. 29-2025

Revenue Regulations No. 29-2025 represents a significant development in the landscape of employee benefits within the Philippines. These regulations aim to offer clarity regarding the taxable and non-taxable elements of employee remuneration, specifically in relation to de minimis benefits. The term ‘de minimis’ refers to benefits that are considered too minor to warrant taxation, thus enhancing employee welfare without substantially impacting tax revenues.

One of the primary purposes of these regulations is to standardize the classification of de minimis benefits that employers may provide to their employees. Not only does this clarify what constitutes such benefits, but it also outlines the limits and types of allowances permissible under the law. For instance, items such as meal allowances, uniforms, and transportation grants can fall under this category, provided they adhere to the stipulated monetary ceilings. By defining these limits, the regulations ensure that both businesses and employees have a clear understanding of what is allowable.

Furthermore, Revenue Regulations No. 29-2025 introduces changes aimed at preventing abuse of the de minimis designation, which can often lead to disputes during tax audits. Businesses should take particular note of the prohibition on including overly generous benefits that exceed the thresholds defined in these regulations, as engaging in such practices could result in tax implications and penalties.

Importantly, the implementation timeline for these regulations is structured to allow businesses a transitional period to adjust to the new guidelines. This adaptability recognizes the need for companies to align their compensation strategies while remaining compliant with Philippine employment laws.

In conclusion, Revenue Regulations No. 29-2025 serves as a crucial framework for understanding employee benefits in the context of Philippine employment, specifically clarifying the role and limits of de minimis benefits in the workplace.

Impacts of Revenue Regulations on Businesses in the Philippines

The implementation of Revenue Regulations No. 29-2025 introduces significant changes that affect both small and medium enterprises (SMEs) and large corporations within the Philippine employment landscape. One of the primary impacts of these regulations is the alteration of tax liabilities for businesses, particularly concerning the de minimis benefits that can now be extended to employees without incurring additional taxes. Previously, businesses faced stricter scrutiny over the allocation of employee benefits, but these new guidelines offer a clearer framework that facilitates compliance.

Moreover, SMEs, which often operate with limited financial resources, are likely to experience a more favorable environment for providing non-monetary benefits to their workforce. The recognition of de minimis benefits can serve as a strategic tool for these smaller enterprises to attract and retain talent in a competitive job market, alleviating some financial burdens associated with higher salaries. Larger corporations may also benefit from improved employee satisfaction and productivity as they adopt these benefits, fostering a more engaged workforce.

In addition to changes in tax liabilities, businesses must also be diligent in revising their compliance requirements. Revenue Regulations No. 29-2025 necessitate that companies adhere to updated reporting standards when declaring de minimis benefits. This requires a thorough understanding of both the definitions provided within the regulations and the need for accurate record-keeping to avoid penalties. A proactive approach in educating management and personnel about these regulations will be crucial in ensuring that companies navigate this transition smoothly.

Furthermore, the emphasis on proper documentation and reporting may lead to increased administrative responsibilities. This shift might disproportionately affect smaller businesses that may lack the resources to manage these new compliance requirements effectively. Therefore, understanding the implications of Revenue Regulations No. 29-2025 is essential for businesses of all sizes, as failure to adapt could lead to unnecessary liabilities and challenges in the prospective workforce market.

De Minimis Benefits for Businesses

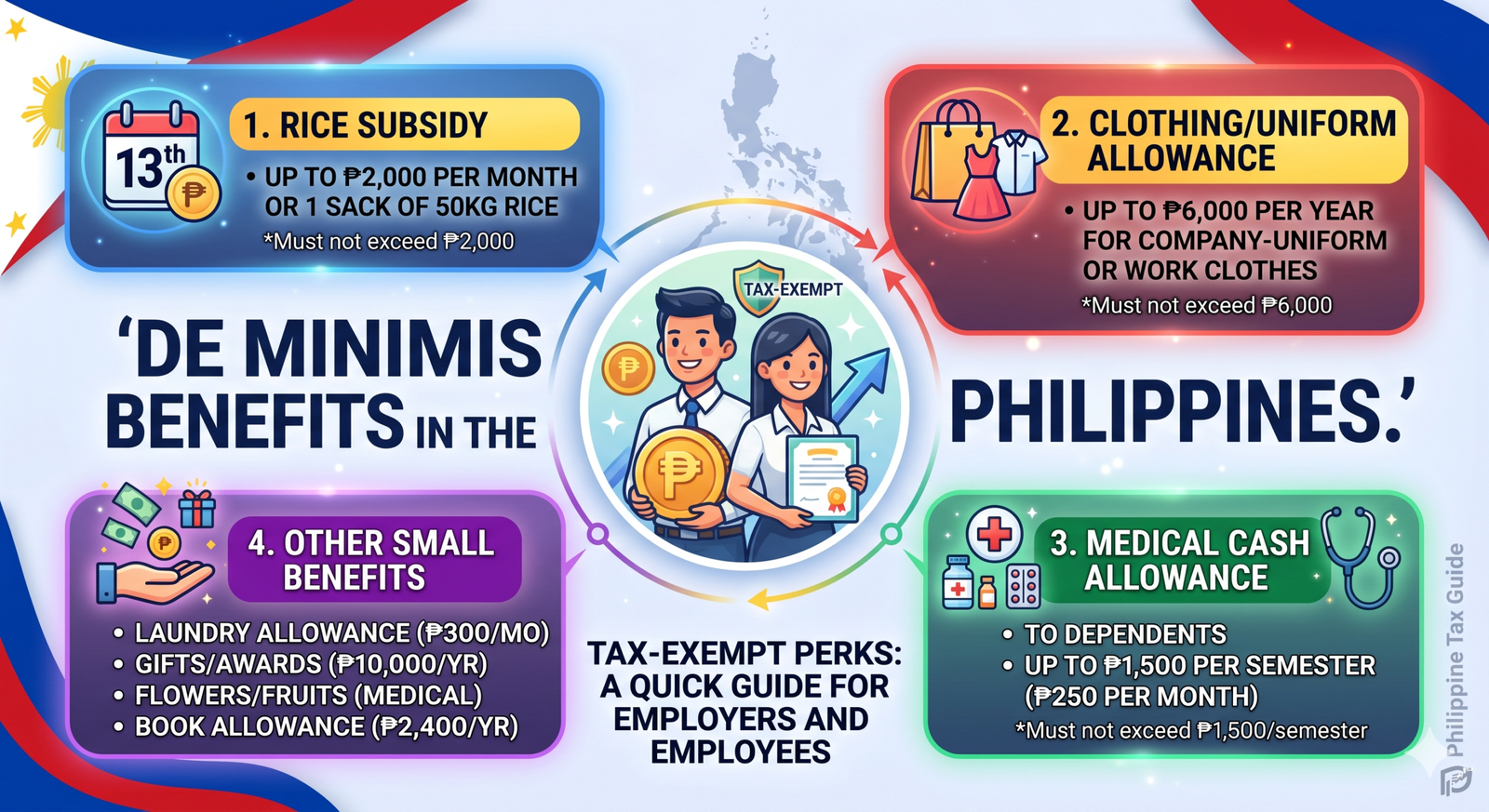

De minimis benefits refer to small-scale allowances that businesses in the Philippines can provide to their employees without incurring tax liability. These benefits are established under Republic Act No. 10963, also known as the Tax Reform for Acceleration and Inclusion (TRAIN) Law. The primary significance of these allowances lies in their potential to foster a more positive workplace environment, thereby enhancing employee satisfaction and retention rates.

Examples of allowable de minimis benefits under Philippine labor laws include gifts during holidays or special occasions, medical assistance, rice subsidy, and transportation allowances. Notably, these allowances can amount up to a total of ₱90,000 annually per employee without being subject to income tax and withholding tax. This provision makes de minimis benefits a strategic advantage for employers looking to enhance their compensation packages.

These allowances serve as an essential component of a comprehensive employee benefits scheme. By maximizing the offer of de minimis benefits, businesses can create an attractive work environment that appeals to both existing and potential employees. Moreover, offering de minimis benefits allows companies to maintain employee morale and motivation, which are critical for ensuring productivity and minimizing turnover.

Furthermore, the tax-exempt nature of these benefits provides a financial incentive for both sides: employees receive a more lucrative compensation package while employers can manage their payroll expenses more effectively. Consequently, adopting a structured approach to implementing de minimis benefits can result in heightened loyalty from employees, which is a long-term asset for any Philippine employment landscape.

How to Utilize De Minimis Advantages

To effectively utilize de minimis benefits in Philippine employment, businesses must first understand the specific allowances permitted under the current legislation, particularly as outlined in Revenue Regulations No. 29-2025. These allowances provide employers an opportunity to offer additional compensation to their employees without the associated tax burdens that typically apply to standard salary increments or bonuses.

One strategic approach is to incorporate de minimis benefits into an employee’s overall compensation package. By doing so, businesses can enhance employee benefits while maintaining compliance with the law. For instance, organizations can offer perks such as subsidized meals, transportation allowances, or health and wellness programs, as these fall within the set limits for de minimis provisions. This not only boosts employee satisfaction and morale but also ensures that both parties minimize their tax liabilities.

Furthermore, clear communication about these benefits is crucial. Employers should regularly inform employees about the de minimis advantages available, ensuring they understand how to maximize these offerings. This can be achieved through company meetings, newsletters, or digital platforms where organizations publish comprehensive guides on employee benefits, focusing on de minimis allowances available under Philippine employment law.

Additionally, regular review and assessment of the de minimis benefits offered can allow businesses to optimize their compensation strategy. For instance, as employees’ needs evolve, the de minimis benefits package can be adjusted accordingly, aligning with the workforce’s preferences and changing economic conditions.

Incorporating de minimis benefits into compensation strategies not only aids compliance with Philippine tax regulations but also promotes overall employee welfare, establishing a supportive work environment essential for long-term organizational success.

Compliance with Revenue Regulations No. 29-2025

To ensure adherence to the Revenue Regulations No. 29-2025 in the Philippines, businesses must take several essential steps aimed at complying with the new de minimis benefits provisions. The primary objective is to maintain an organized system that accurately reflects employee benefits, particularly as it pertains to the categorization of de minimis benefits under the updated regulations.

A sound strategy begins with a thorough understanding of the criteria for qualifying benefits. Employers need to familiarize themselves with the specific types of benefits recognized as de minimis as outlined in the regulations. It is critical to train human resource personnel on these classifications to ensure that employee benefits are managed effectively. Employers should consider implementing a dedicated policy for de minimis benefits that delineates eligible benefits, limits, and processing procedures.

Maintaining accurate records is paramount in demonstrating compliance. Businesses should establish reliable systems for tracking each employee’s de minimis benefits. This could involve integrating payroll systems with benefit management tools to automate the collection and reporting of these benefits, thereby minimizing errors and making audits more manageable.

Filing requirements also play a crucial role in compliance. Businesses must ensure that they are prepared to submit necessary documentation to the Bureau of Internal Revenue (BIR) and keep records for the required retention period. This includes preparing timely and accurate Statements of Employee Benefits that explicitly detail de minimis amounts given to employees during the fiscal year.

Lastly, it is advisable to consult with tax professionals or legal advisors who specialize in Philippine employment law to interpret the regulations effectively and assist in the implementation of best practices. This approach will not only facilitate compliance with Revenue Regulations No. 29-2025 but also enhance the management of employee benefits overall.

Case Studies: Successful Implementation of De Minimis Allowances

In recent years, various businesses across the Philippines have embraced de minimis allowances as part of their employee benefits strategy. These allowances refer to non-taxable benefits that enhance the overall compensation package for employees, which can lead to increased job satisfaction and retention rates.

One notable case is a leading manufacturing company that integrated de minimis benefits to augment its employee compensation structure. By offering transportation allowances, meal vouchers, and health-related benefits, the company observed a significant boost in employee morale. Consequently, their productivity increased by approximately 15%, indicating that the de minimis benefits had a positive impact on workforce efficiency. Additionally, employee turnover rates decreased, suggesting that these non-monetary benefits fostered a greater sense of loyalty among staff.

Another example is a tech startup that implemented a flexible work-from-home policy supported by de minimis allowances, which covered utility expenses for remote workers. This initiative not only attracted top talent in a competitive industry but also resulted in higher employee engagement. Surveys conducted showed a 20% increase in job satisfaction, with employees feeling valued and recognized by the organization. This proved instrumental in creating a productive work environment and contributed to the company’s reputation as an employer of choice.

A retail enterprise also adopted de minimis allowances by providing additional benefits such as discounts for staff purchases and wellness programs. The implementation of these employee benefits not only improved staff morale but also translated into better customer service, enhancing the shopping experience for clients. The company reported increased sales and customer satisfaction scores, indicating that the positive impacts of de minimis benefits extended beyond the workplace and into the realm of business performance.

Through these diverse examples, it is evident that the strategic use of de minimis allowances can yield significant advantages for Philippine businesses, reinforcing the importance of employee benefits in driving overall organizational success. The positive outcomes underline the effectiveness of such allowances in fostering a motivated and loyal workforce tailored to meet the unique challenges of the Philippine employment landscape.

Challenges and Considerations for Businesses

As Philippine businesses navigate the incorporation of de minimis benefits into their employment structures, a variety of challenges and considerations emerge that could impact national compliance and employee satisfaction. The de minimis provisions, as per Revenue Regulations No. 29-2025, necessitate thorough adjustments across multiple business functions, particularly in accounting and human resources.

From an accounting perspective, integrating de minimis benefits requires precise understanding and documentation. Businesses must ensure that employee benefits align with the definition of de minimis as outlined by the regulations. This entails rigorous evaluation of existing benefits packages, adaptation of payroll systems, and potential restructuring to encompass additional non-taxable benefits. Compliance with intricate labor laws while avoiding potential penalties or misclassifications adds layers of complexity for financial teams.

Human resources departments are equally challenged as they must communicate and educate employees about the newly established de minimis provisions effectively. This involves clarity on which benefits qualify and how they will be integrated into existing employee benefits schemes. Further, treating these adjustments sensitively is vital to maintain employee morale and trust, as some advantages might shift or evolve under these regulations.

Strategic planning is another crucial area that businesses must focus on when adapting to these regulations. Leadership must evaluate how de minimis provisions fit into overall employee value propositions and align with organizational goals. This includes positioning de minimis benefits as a recruitment tool while ensuring that the offerings remain competitive within the industry. Balancing cost management with attractive employee benefits underlines the necessity for thorough market analysis and projections to anticipate returns on investment.

In conclusion, while the de minimis benefits framework under Philippine employment laws presents exciting opportunities, it equally poses substantial challenges that require comprehensive planning and implementation efforts across accounting, human resources, and strategic management functions.

Conclusion and Future Outlook

In reviewing the key aspects of de minimis benefits and the recently established Revenue Regulations No. 29-2025, it is essential to recognize their importance in the Philippine employment landscape. De minimis benefits serve as a substantial avenue for employers to provide non-taxable compensation to employees, which significantly bolsters employee morale and productivity. The updated regulations clarify the scope and nature of these benefits, ensuring a better understanding and implementation by businesses operating in the Philippines.

Moreover, the regulatory framework introduced by Revenue Regulations No. 29-2025 aims to streamline the provision of these benefits while reinforcing compliance within the sector. Employers are encouraged to familiarize themselves with the specifics of these regulations to optimize how they categorize and deliver employee benefits. With proactive engagement, businesses can effectively align their incentives with the dynamic requirements of the workforce.

The evolving economic climate necessitates that businesses remain agile and responsive, particularly when it comes to adhering to legislative changes. The implications of these regulations underscore the need for businesses to integrate de minimis benefits into their HR policies strategically. This not only sustains employee satisfaction but also promotes compliance with the tax obligations laid out by the Bureau of Internal Revenue.

Looking ahead, as the regulatory environment continues to evolve in the Philippines, organizations should be prepared to adapt their employee benefits packages accordingly. Staying informed regarding potential updates and best practices will enable firms to navigate the complexities of Philippine employment regulations proficiently, ensuring that they remain competitive while fostering a positive workplace culture.