We make resolutions at the beginning of each year—promises to break bad behaviors. Most of the time, those resolutions are discreetly carried over from one year to the next, recycled, and put off.

This tendency has also affected Philippine tax policy. Due to inflationary pressures and growing living expenses, it has long been clear that the ceilings for de minimis benefits needed to be reviewed; yet, these thresholds remained largely unaltered for years.

The Bureau of Internal Revenue (BIR) has finally taken action to revise the non-taxable ceilings for these benefits as of January 6, 2026, with the release of Revenue Regulations (RR) No. 29-2025. The regulation is a timely way to start the year and represents a little but significant improvement.

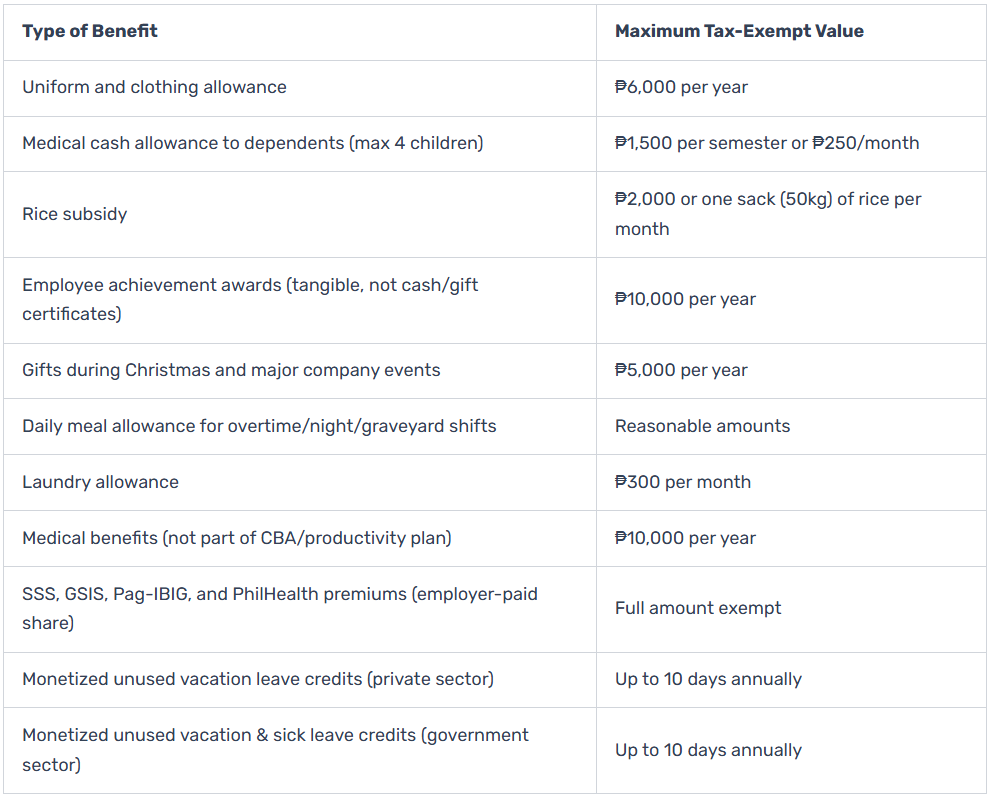

De minimis benefits are relatively inexpensive amenities and perks that employers provide to staff members in order to foster efficiency, goodwill, health, or contentment. As long as they don’t exceed the specified caps, these benefits are free from income and withholding taxes.

The following tax-exempt de minimis benefit ceilings are raised by RR 29-2025:

Even while the changes to the individual ceilings might not seem like much, the rise in permitted non-taxable amounts can have a considerable financial impact when taken into account cumulatively—across several benefit categories and over the course of a year.

Designing strategic benefits: An chance for planning

RR No. 29-2025 offers companies a strategic chance to reevaluate the structure of compensation. It creates more room for a more careful salary and benefits structure, even though it doesn’t actually raise salaries. This enables firms to enhance total employee wellbeing by providing tax-efficient, non-taxable benefits in addition to wage changes.

Payroll expenses are compounded and permanent as a result of widespread salary increases. These have an impact on future compensation bases, statutory contributions, and withholding taxes. On the other hand, appropriately constructed de minimis benefits—within specified ceilings—give employers more freedom to offer specific, non-taxable assistance without correspondingly raising withholding tax requirements.

Employers and employees can both profit from rerouting a part of planned compensation changes into acceptable de minimis benefits. This results in increased effective take-home pay for workers and maintains the tax-exempt status of benefits that directly meet their everyday needs. This strategy can assist organizations in lowering additional additional payroll expenses. Additionally, a well-thought-out de minimis benefits scheme can increase productivity and enhance employee morale and retention.

Benefits like rice subsidies and medical cash allowances, for example, might reduce everyday costs. Making these benefits more accessible in a non-taxable form, in my opinion, shows a company’s dedication to the welfare of its workers.

Should more de minimis benefits be acknowledged beyond higher ceilings?

In addition to updating current ceilings, RR No. 29-2025 poses a more general question: Should the de minimis framework be expanded to legally identify more shared benefits?

Transportation reimbursements and technology or connectivity support, which have grown essential in an increasingly digital world, are two examples. Subject to acceptable boundaries, recognizing such goods under the de minimis framework would acknowledge costs that employees currently frequently incur rather than creating new kinds of remuneration.

Expanding de minimis benefits to cover such daily necessities could be viewed as a practical compromise given the difficulties in enacting minimum wage hikes. Compared to wage legislation, modifications to the de minimis framework provide a more adaptable option that is relatively simpler to implement. These steps offer a useful means of providing employees with focused assistance, but they do not replace more comprehensive labor reforms or equitable salary changes.

A final insight: incremental yet significant

RR 29-2025’s modifications are sensible and obviously appreciated. The new ceilings may still not accurately reflect current inflation levels, though, given that these criteria were left unaltered for a number of years and then only slightly modified.

However, the regulation’s importance shouldn’t be undervalued, even though it might not have the same broad effects as other recent policies like the VAT regulations on digital services. All employers and workers are typically impacted by changes to de minimis ceilings, regardless of industry or company size. Because of this wide scope, even little changes have significant effects on cost control, payroll compliance, and compensation planning.

In order to stay ahead of economic realities, we expect that the BIR would continue to regularly review the de minimis framework, either by recognizing new advantages over time or by making periodic modifications to current ceilings. Similar to a New Year’s resolution, the true worth of this change is found in the commitment to review and improve it over time rather than just making one change.